ATTENTION: First Home Buyers

Auction clearance rates are falling. House prices are softening.

The market is shifting and opportunities like this don’t stay open for long.

If you've been waiting until you have a 20% deposit saved, you could be delaying your property journey unnecessarily. There are options available that may allow you to buy with as little as 5%, 2%, or even 0% deposit, depending on your circumstances.

While many buyers are sitting on the sidelines, those who act now could be in a stronger position to secure the right property before competition returns.

Book your strategy session today and find out what’s possible for you before the market moves again.

Investors are pulling back. First Home Buyers should be paying attention.

Recent Federal Budget changes have reduced investor activity, creating a unique opportunity to enter the market with less competition.

Waiting could mean competing against more buyers in the future and paying more for the same property.

We help First Home Buyers understand their options, build a smart buying strategy, and create a plan to become mortgage-free sooner.

Don't miss the opportunity that's in front of you today.

Book your strategy session now.

CLICK BELOW TO WATCH FIRST!

The biggest mistake First Home Buyers make is assuming they're not ready.

You may already qualify for options that could get you into the market sooner than you realise but you'll never know until you check.

Every day you delay is another day of missed opportunities.

Complete the questionnaire below now to secure your Discovery Call and find out exactly what's possible before the market changes again.

TESTIMONIALS

What others are saying

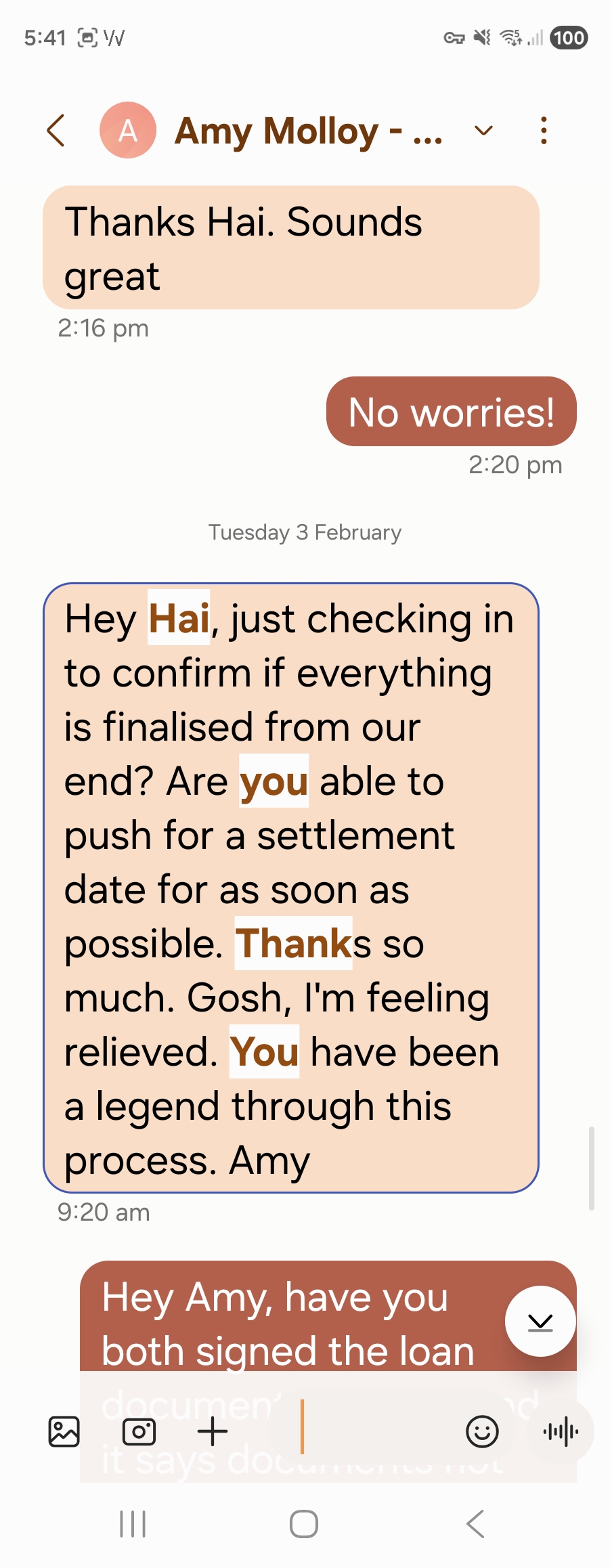

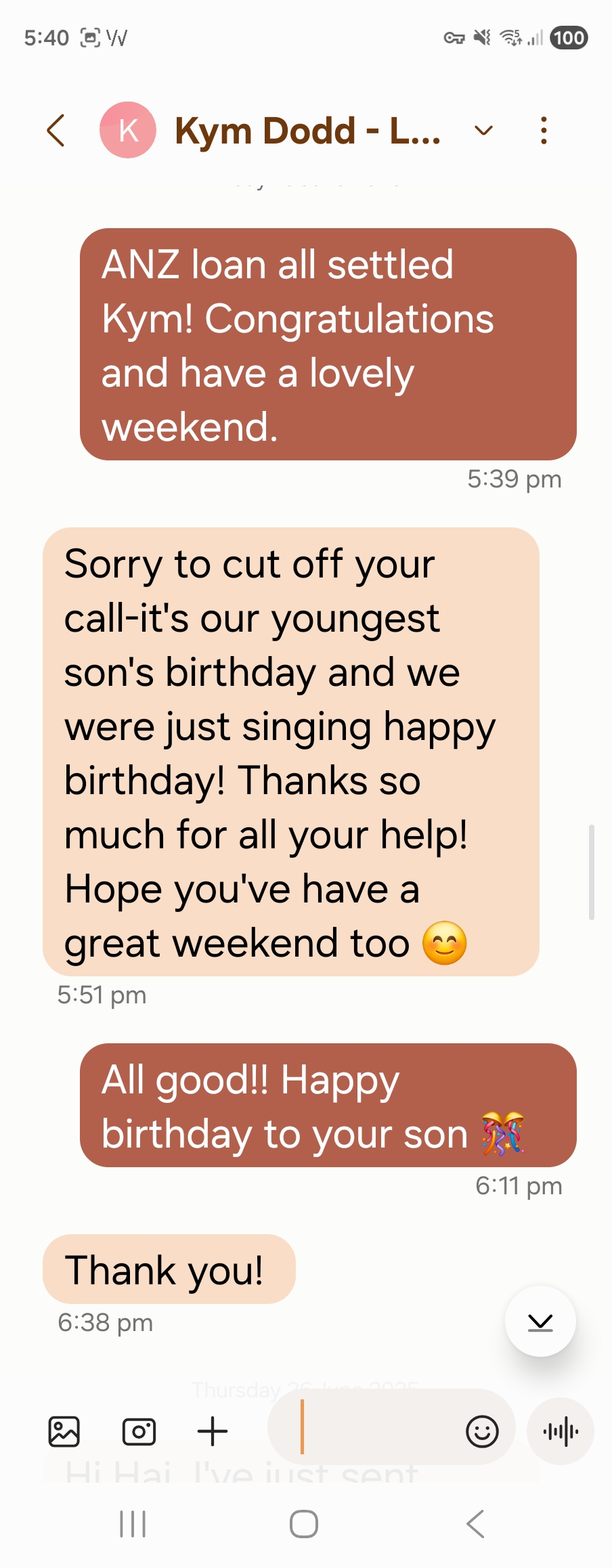

Client's text after approval / settlement

Our team. We have two brokers and two support staff.

First Home Buyers(left) and Financial Planner and Accountant we share an office with on the right

For First Home Buyers Who Need a Clear Path to Home Ownership

Stamp Duty Concessions

Home Guarantee Scheme

First Home OWners Grant

Guarantor loans

Low deposit lending

self employed and payg borrowers

Click apply to get started

STILL NOT SURE?

Frequently Asked Questions

Here's what we usually get asked

How do I get started working with you?

Fill out the questionaire above to make a discovery call booking.

So how does it work?

We start with a Discovery Call to understand your situation and determine whether we're the right fit for each other.

From there, we'll conduct a Strategy Session to map out your current position, future goals, and create a clear plan to help you purchase your first home.

We'll identify the loan features that matter most to you, research suitable lending options, and recommend a solution aligned with your goals.

Most importantly, we'll show you proven strategies to reduce the amount of interest you pay and create a plan to help you pay off your mortgage sooner, saving you time and money over the life of your loan.

What schemes are available to me as a First Home Buyer?

This would depend on the state you are in and the type of property you are buying.

You may qualify for stamp duty concessions, home guarantee scheme (no lenders mortgage insurance) or First Home Owners Grant.

Why should I work with you?

We've helped over 100 families and individuals buy their first home.

As former first home buyers ourselves, we understand the challenges that come with the journey. That's why we focus on making the process simple, stress free, and easy to navigate from start to finish.

Why shouldn't I just go direct to the bank?

When you rely on just one bank, you're limited to their lending policies, borrowing capacity calculations, and property valuations.

Not all lenders participate in the Home Guarantee Scheme, which could mean paying Lenders Mortgage Insurance when you may not need to. Lending policies also vary significantly between banks, and being declined by one lender doesn't necessarily mean you can't be approved elsewhere.

A second opinion could save you thousands of dollars and potentially increase your borrowing power, giving you access to more opportunities when purchasing your first home.

How else can you help me?

Buying a property involves more than just securing a loan.

That's why we provide access to a trusted network of professionals, including conveyancers to manage your settlement, financial planners to help protect your financial future and review your insurance needs, and buyers agents who can assist you in finding and securing the right property.

Our goal is to ensure you have the right team around you at every stage of your property journey.

How have you helped First Home Buyers in the past?

One of our first home buyer clients came to us after being declined by her bank, with just six business days remaining to secure finance approval or risk losing her $25,000 deposit.

She had worked incredibly hard, holding down two jobs to achieve her goal of home ownership. Her bank refused to recognise the income from her second job, significantly reducing her borrowing capacity.

We quickly identified a lender whose policy allowed them to accept both income sources. Within less than a week, we secured formal finance approval.

The reality is that every lender has different policies. Being declined by one lender does not mean you cannot be approved elsewhere. Finding the right lender can make all the difference.

I'm self employed and haven't got 2 years financials or tax returns, can you still help?

Yes, there may still be options for you. Otherwise, we can create a plan to help you get there.

I have a low deposit, can you still help me?

There are many options for First Home Buyers. We might still be able to help. You can get away with a 5% deposit or sometimes even 0%(If you have a guarantor or the deposit can be gifted).

How many lenders do you work with?

We work with over 40 different lenders.

Can you recommend what type of property to buy?

No, we only assist with the finance side of your loans. However, if you need help finding a property, we can connect you with our recommended buyer’s agents who have achieved great results for many of our clients.

I just started a new role, do I have to wait three months?

No you might not need to. We have lenders that can accept your employment contract.

Do you charge a fee?

No, we are generally paid by the lender. The only time a fee may apply is for more complex applications, such as businesses with multiple entities, applications involving more than two applicants, or other non standard lending scenarios.

My bank/broker told me I can't borrow anymore, can you help?

We have helped many clients who were previously told they could not borrow any further. Getting a second opinion can make all the difference.

I have bad credit, can you still help?

Sometimes we can still get these loans through depending on how bad it is. We can also help connect you with a credit repair specialist.

Ready to get started? Click apply and fill out the questionnaire.

How We Help First Home Buyers

Step 1 - Strategy Session

We take a deep dive into your current position, work out your current and future goals and create a plan to purchase your First Home.

Step 2 - Lender Recommendation

We start by understanding what you want from your home loan, then research and compare lenders to find the most suitable option for your situation. We'll provide a recommendation and explain the reasoning behind it, so you can make an informed decision. The choice is always yours. We're simply here to guide you through the process and help you secure the right loan with confidence.

Step 3 - Mortgage Repayment Strategies

We'll go through ways you can reduce the interest charged and pay down your home loan quicker. Our goal is to make you debt free.

MEET THE FOUNDER

Hey, I'm Hai, founder of J2W Finance

Achievements

$300,000,000+ loan settlements

Owner of a small mortgage broking business with 4 staff

Helped over 100+ First Home Buyers

10 years+ experience

100+ five star reviews

Father of three cheeky boys (including my corgi)

Chelsea supporter - LONDON IS BLUE